IRENA 2024/25: Clear Figures and Keys for Latin America

Solar and wind energy are arriving with favorable figures. In LATAM, they need clear policies and technological updates to support them

The International Renewable Energy Agency (IRENA) has published its latest report, “Renewable Power Generation Costs in 2024/2025,” which analyzes the cost evolution of key renewable technologies globally and their role in the energy transition.

One of the central findings is that the average cost of solar photovoltaic (PV) and onshore wind power continues to decline, making them the cheapest sources for new installations in most markets. Offshore wind and concentrated solar power (CSP), although still having higher costs, show sustained improvements thanks to technological innovations, economies of scale, and more efficient installation processes.

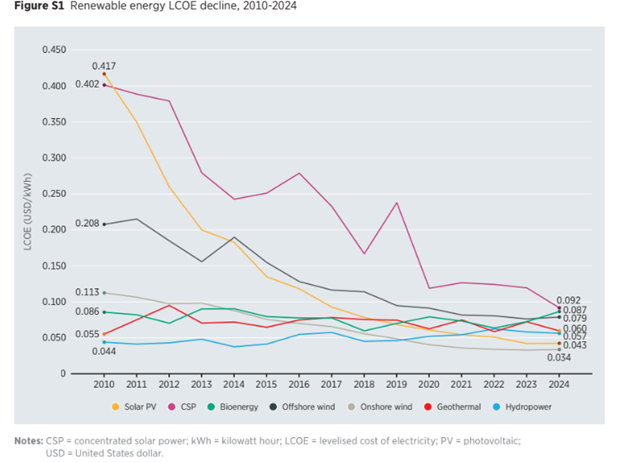

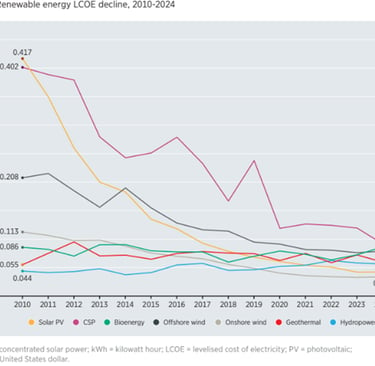

The study also highlights their competitiveness against fossil fuels: across most of the world, the levelized cost of electricity (LCOE) for renewables is below that of new gas and coal plants. This reinforces the idea that investing in renewables is no longer just an environmental decision, but also an economically rational strategy. The chart below shows how the LCOE has been reduced over the years.

Another key aspect is regional heterogeneity. Countries with greater resources achieve record low costs, while in emerging markets, financial risks raise capital costs and increase the LCOE. This demonstrates the importance of generating accessible financing conditions and stable policies to accelerate renewable deployment worldwide.

Looking ahead to 2025, IRENA projects that solar PV will continue to become cheaper, and offshore wind will play a growing role in Europe and Asia, with progressive cost reductions. Furthermore, technologies like geothermal and bioenergy are beginning to occupy strategic positions in the diversification of energy matrices.

The region has abundant resources, but the cost of money, exchange rates, and saturated transmission can erase the advantage. The path forward includes: Batteries to reduce energy peaks, digital tools to better dispatch every MWh, and hybrid projects that leverage the same interconnection. If accessible financing, clear rules, and met connection dates are added, competitiveness reaches the user.

In conclusion, the IRENA report provides a solid economic argument for incorporating new capacity, especially in developed economies, where cheap capital and mature grids allow for the full capture of that cost advantage. In developing economies, the challenge is to close the financing gap and accelerate infrastructure. The next stage is enabling: competitive financing, storage, and digitalization that provide flexibility, and grids capable of integrating more generation without bottlenecks.

Source: IRENA, “Renewable Power Generation Costs in 2024/2025”

As renewable capacity grows in the coming years to meet climate goals, enabling technologies such as battery storage, digitalization, and hybrid systems will become increasingly vital for integrating variable renewables, improving asset performance, and enhancing grid response. Although challenges persist—access to financing, permit delays, supply chain bottlenecks, and geopolitical risks—greater alignment among policy, regulation, and investment is essential to accelerate the transition.

North Delegation

Federico Rossi 600 - Yerba Buena, Tucumán, Argentina

+54 9 11 6422-0088

info@smartenergysolutions.com.ar

Subscribe for the latest news

South Delegation

Los Pinos 1758 - Cipoletti, Río Negro Argentina

+54 9 11 6438-8507

info@smartenergysolutions.com.ar